Managing a global supply chain in 2026 involves more than logistics. Success now depends on how effectively an organization navigates escalating geopolitical tensions and rapidly shifting regulations.

These pressures directly impact the strategic objectives of C-suite leaders, making real-time visibility and automated mitigation essential for maintaining margins.

Review the supply chain statistics below to see how these external factors are reshaping operations. Sourced from industry benchmarks and Tradeverifyd proprietary surveys conducted in 2025-2026, they provide the data needed to identify hidden risks and find opportunities for a long-term strategic advantage.

Key takeaways:

73% of supply chain leaders expect to hit their tariff absorption wall by the end of 2026, the point at which costs must shift from corporate balance sheets to consumer invoices.

While 93% of executives report high confidence in their oversight, only 56% of organizations can trace material origins to Tier-3 or Tier-4 sources.

Automated mitigation has transitioned from a future goal to a baseline requirement, with 72% of supply chain executives stating it is now mandatory for managing modern disruptions.

Resilience is a primary focus, as major supply chain interruptions lasting a month or longer occur on average every 3.7 years, often driven by extreme weather or geopolitical volatility.

Efficiency remains the top driver for technology investment as U.S. business logistics costs climb to $2.58 trillion, representing 8.8% of the national GDP.

Supply Chain Management Statistics

Gaining insights into supply chain management allows your company to create a healthier, more effective process.

These statistics examine the integrated performance of supply chains from planning and sourcing to delivery and the importance of ongoing analysis. See how your initiatives compare to others, and gain insight into what changes could benefit your operation.

73% of supply chain leaders expect to hit their tariff absorption wall by the end of 2026, the point at which costs must shift from corporate balance sheets to consumer invoices. (Tradeverifyd, 2026)

83% of organizations currently absorb at least a portion of tariff costs internally, with 46% absorbing nearly all of these costs to maintain price stability. (Tradeverifyd, 2026)

Only 12% of companies currently pass the majority of tariff costs directly to customers, highlighting the extreme pressure on modern corporate margins. (Tradeverifyd, 2026)

49% of supply chain leaders identify escalating transportation expenses as the most significant external pressure facing their operations. (Tradeverifyd, 2026)

44% of logistics executives view increasing consumer demand for transparency as a primary driver of their current corporate strategy. (Tradeverifyd, 2026)

In the semiconductor sector, the primary driver for visibility tool upgrades is efficiency and cost reduction (35%), rather than increasing operational agility. (Tradeverifyd, 2025)

U.S. business logistics costs reached $2.58 trillion, equaling 8.8% of the national GDP. (Penske, 2025)

M&A deal value in advanced industries nearly doubled in 2025 compared to the previous three-year average, driven by aerospace and semiconductor vertical integration. (McKinsey & Company, 2026)

As of 2025, a record 52% of total buyout-backed inventory has been held for more than four years, signaling a backlog in the exit market for industrial assets. (McKinsey & Company, 2026)

In 2025, 69% of 3PLs reported increased profitability, largely due to gains in efficiency from AI and automation. (Inbound Logistics, 2025)

The Global Supply Chain Pressure Index (GSCPI) rose to 0.49 in February 2026, reflecting an 18.7% increase in pressure from the prior month. (Federal Reserve Bank of New York, 2026)

Average terminal dwell time for rail containers in the U.S. saw a year-over-year decrease of 5% in January 2025 from January 2024. (EY, 2026)

As of late 2025, there were approximately 409,000 unfilled positions in U.S. manufacturing, with the industry projected to face a gap of 1.9 million unfilled roles by 2033. (Deloitte, 2025)

35% of respondents in the MHI/Deloitte 2025 report ranked workforce and talent shortages as the third most impactful supply chain trend. (MHI, 2025)

38% of manufacturers planned on launching re-skilling initiatives in 2025, a significant climb from the 25% reported just one year earlier. (MHI, 2025)

At the 2025 CPO Summit, over half of all CPOs expressed urgent concern that their organizations are being directly and negatively impacted by evolving global tariffs. (EY, 2025)

26% of CEOs identify "Achieving sustainability targets" as one of their top three most important transformation outcomes for the year. (EY, 2026)

Automation and AI Statistics

The overall market value for automation and AI within the supply chain continues to grow. By examining automation and AI statistics, your team can better understand rising competitors’ efficiency, identify proven use cases, and pin down the best time for adoption.

72% of supply chain executives believe that automated mitigation capabilities are now mandatory for successfully navigating modern market disruptions. (Tradeverifyd, 2026)

69% of compliance and supply chain teams spend 11 or more hours each week on manual data translation to standardize formats for regulatory submissions. (Tradeverifyd, 2026)

48.7% of surveyed organizations have transitioned away from manual data management to adopt AI-powered predictive analytics for their daily workflows. (Tradeverifyd, 2026)

27% of executives identify fragmented IT and systems integration as the primary barrier to achieving Digital Product Passport (DPP) readiness. (Tradeverifyd, 2026)

67% of enterprises report that despite increasing their financial commitment to visibility tools, the return on investment has stalled due to the continued use of fragmented legacy systems. (Tradeverifyd, 2026)

52.4% of semiconductor firms currently use AI specifically for quality control and defect detection. (Tradeverifyd, 2025)

63% of auto leaders believe the ability to model supply chain impact is the most transformative technology for the next 3-5 years (Tradeverifyd, 2025).

67% of business leaders identify AI as a recession-proof investment, stating they will maintain or increase spending even during economic downturns. (KPMG, 2026)

86% of C-suite leaders feel prepared to increase their investment in AI in 2026. (Accenture, 2025)

78% of those C-suite leaders view AI as more beneficial to revenue growth than simple cost reduction. (Accenture, 2026)

78% of manufacturers allocate over 20% of their overall improvement budgets toward smart manufacturing initiatives. (Deloitte, 2025)

88% of manufacturers anticipate smart manufacturing investments will continue or increase in the next fiscal year. (Deloitte, 2025)

59% of executives expect to see measurable ROI from AI integrations within 12 months. (KPMG, 2026)

86% of executives plan to invest in AI and advanced analytics for cost reduction purposes across customer service, sales, marketing, and supply chains in 2025. (BCG, 2025)

Global tech spending is projected to grow by 7.8% in 2026, reaching a total of $5.6 trillion. (Forrester, 2026)

Software and IT services are expected to constitute 66% of global tech spend in 2025. (Forrester, 2025)

29% of manufacturers are currently using AI/machine learning (AI/ML) at the facility or network level. (Deloitte, 2025)

AI adoption is predicted to nearly triple from 28% today to 82% within the next five years. (MHI, 2025)

37% of manufacturers rank robotics/physical automation as a top 1 or 2 investment priority for the next two years. (Deloitte, 2025)

46% of manufacturers rank process automation as a top 1 or 2 investment priority for the next two years. (Deloitte, 2025)

55% of supply chain leaders are increasing their overall technology innovation spending, with 60% planning to invest over $1 million. (MHI, 2025)

34% of manufacturers prioritize investment in active sensors over the next 24 months. (Deloitte, 2025)

Predicted five-year adoption for inventory and network optimization is 92%. (MHI, 2025)

The predicted 5-year adoption rate for autonomous vehicles and drones is 64%. (MHI, 2025)

Smart manufacturing initiatives reported average productivity improvements of 7% to 20% in 2024. (Deloitte, 2025)

43% of employees state that clear, comprehensive training would be the single most effective factor in increasing their confidence using AI tools. (Accenture, 2026)

As of 2025, only 27% of companies have successfully introduced AI into their procurement or supply chain functions, with 14% of organizations still lacking any digital roadmap. (Inspectorio, 2025)

Procurement and Supplier Statistics

Your supply chain depends on a network of suppliers and vendor relationships at every tier. By improving your processes within this area, you can better identify high-spend categories, reduce maverick spend, and pinpoint bottlenecks. Procurement and supplier statistics offer additional insights to strengthen your supplier relationships.

93% of executives report high confidence in their overall oversight, yet this same group identifies Tier 2 and Tier 3 suppliers as their most critical operational blind spots. (Tradeverifyd, 2026)

Only 56% of supply chain organizations have the capability to trace material origin and batch-level information down to Tier-3 or Tier-4 sources. (Tradeverifyd, 2026)

Just 49% of enterprises report that at least half of their Tier-1 supplier base is currently confirmed to provide DPP-compliant data ahead of 2027 requirements. (Tradeverifyd, 2026)

67% of firms increased their financial commitment to visibility tools over the last 12 months, yet a lack of seamless data integration with external partners remains a primary barrier to procurement success. (Tradeverifyd, 2026)

70% of semiconductor manufacturers plan to deploy advanced mapping and visibility platforms before the end of the 2026 fiscal year to address sub-tier vulnerabilities. (Tradeverifyd, 2025)

Just 17.7% of semiconductor professionals say they are extremely confident in their Tier 2 and Tier 3 visibility. (Tradeverifyd, 2025)

43.5% of auto suppliers are only moderately confident in the ability of their sub-tier suppliers to meet quality expectations (Tradeverifyd, 2025).

The top three value drivers influencing procurement strategy globally are value/savings, supplier performance, and supplier resiliency. (EY, 2025)

Cost management remains the most critical priority for one-third of corporate leaders globally in 2025, up eight percentage points from 2024. (BCG, 2025)

86% of supply chain executives plan AI/analytics investments for cost reduction across the supply chain. (BCG, 2025)

As of 2025, the top priority for supplier diversity leaders has shifted to economic impact and supply chain competitiveness (64%), with teams prioritizing resilience over basic spend tracking. (Supplier, 2025)

33% of procurement organizations are specifically increasing their focus on raw data quality and integrity as they move away from manual supplier verification models. (Supplier, 2025)

Despite a shifting political landscape, 87% of global executives report steady or growing support for their supplier diversity programs in 2025. (Supplier, 2025)

86% of CPOs are prioritizing category management and strategic sourcing as the primary vehicle for delivering long-term ESG and sustainability value. (EY, 2025)

Companies that fail to meet cost targets tend to underperform peers on total shareholder return by an average of nine percentage points. (BCG, 2025)

Supply Chain Disruption and Risk Statistics

Your supply chain's risk significantly impacts the services you provide to your customers. Global supply chain disruptions can decrease customer satisfaction, and the costs can be hefty. Beyond traditional factors, elements such as cybercrime are rising. Analyzing risk and disruption statistics can help your organization stay ahead, offering insights into potential problems and solutions.

60% of supply chain leaders say a 10% tariff increase would force them to implement immediate price hikes to offset the risk. (Tradeverifyd, 2026)

53% of supply chain leaders report only partial confidence in their ability to quantify tariff exposure across their multi-tier networks accurately. (Tradeverifyd, 2026)

41% of high-tech supply chain professionals identify geopolitical volatility and export controls as their greatest risk concern for the coming year. (Tradeverifyd, 2025)

21% of leaders currently operate without real-time visibility into disruptions affecting their suppliers, while 18% are unable to identify which suppliers pose the highest regulatory or compliance risk. (Tradeverifyd, 2026)

39% of organizations currently list the fluctuating impact of international tariffs as a high-priority risk factor within their procurement frameworks. (Tradeverifyd, 2025)

46% of semiconductor companies still rely on manual spreadsheets to track supply chain risks. (Tradeverifyd, 2025)

77% of automotive suppliers consider real-time event notifications to be extremely or very important for their operations (Tradeverifyd, 2025)

42% of executives cite a lack of real-time data as their main limitation when responding to a disruption. (Tradeverifyd, 2026)

Supply chain disruptions lasting longer than one month happen, on average, every 3.7 years. (McKinsey & Company, 2020)

In 2025, extreme weather became the single largest cause of supply chain disruption for the first time in nearly a decade, surpassing even cyber-related outages. (BCI, 2025)

77% of executives reported their company was negatively impacted (to some or a great extent) by compliance complexity. (PwC, 2025)

US–China trade fell by approximately 30% in 2025, with US tariff rates reaching their highest levels since World War II. (McKinsey, 2026)

$165 billion in trade was pushed away from the US–China corridor in 2025, reorienting toward new geopolitical partners and regional hubs. (McKinsey, 2026)

71% of U.S. CEOs plan to alter supply chains over the next three to five years, partly due to trade uncertainties. (Deloitte, 2025)

By the third quarter of 2025, 78% of manufacturers identified trade policy uncertainty as their primary business concern, with companies expecting input costs to rise by an average of 5.4% annually. (Deloitte, 2026)

31% of global executives reported having already launched contingency plans related to tariffs and regulatory changes following the U.S. election. (BCG, 2025)

Inflation (38%) and economic uncertainty (37%) ranked as the top two most impactful supply chain trends for 2025. (MHI, 2025)

In 2025, the average cost of a data breach for U.S.-based organizations reached a record $10.22 million. (IBM, 2025)

Cybersecurity (51%) and data protection/privacy (51%) ranked as joint top compliance risk priorities. (PwC, 2025)

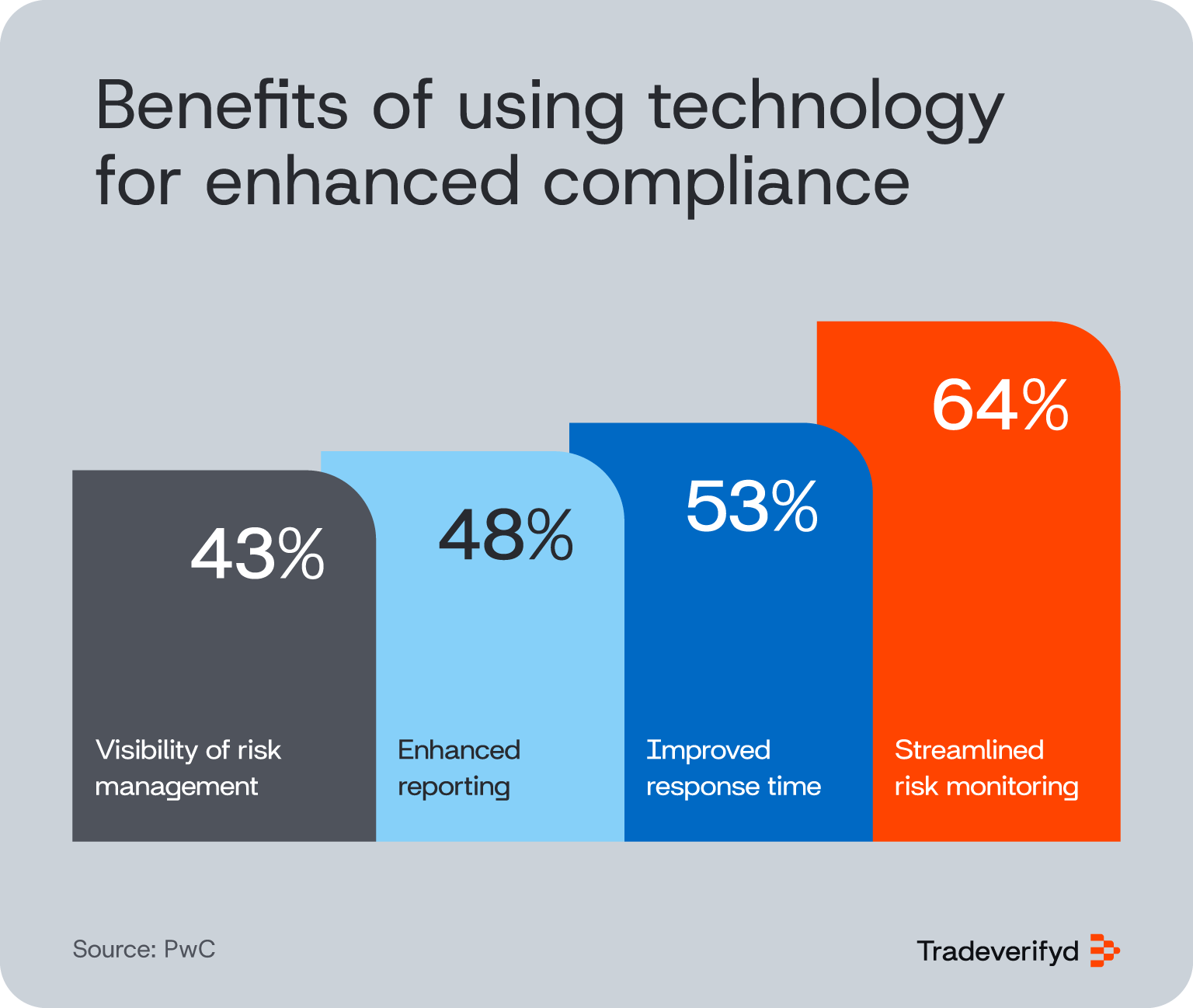

Companies using technology for compliance report better risk visibility (64%), faster issue identification/response (53%), and increased productivity/cost savings (43%). (PwC, 2025)

What’s Next for Your Supply Chain

Managing a supply chain is a complex challenge, from sourcing raw materials to delivering to customers or retailers. Analyzing current supply chain statistics enables an organization to learn from market shifts and make data-driven adjustments rather than relying on trial and error.

Based on recent figures and trends, here are a few takeaways for every company operating within the global supply chain.

Address talent gaps and efficiency gaps

Tradeverifyd research shows that 69% of compliance and supply chain teams spend 11 or more hours every week on manual data translation.

Karyl Fowler, Chief Policy Officer at Tradeverifyd, identifies data literacy, cross-functional collaboration, and technology fluency as the most critical skill gaps facing the 1.9 million unfulfilled roles in the industry. She suggests bridging these gaps by "partnering with external platforms or consultants to embed new capabilities into workflows”.

Prepare for the tariff absorption wall

73% of supply chain leaders expect to hit their tariff absorption wall by the end of 2026, the point where internal margins can no longer offset trade costs. With U.S. business logistics costs reaching $2.58 trillion, efficiency is a requirement for survival. Organizations should focus on strengthening procurement strategies and on using third-party data to gain visibility into sub-tiers where hidden costs often reside.

Prioritize unified technology investments

48.7% of organizations are already moving away from manual data management to adopt AI-powered predictive analytics. While 71% of C-suite leaders are prioritizing digital tools to manage change, success is often stalled by fragmented legacy systems. Fowler emphasizes focusing on "data quality, governance, change management, and precise use case definitions" to ensure technology investments deliver measurable ROI.

Prepare for the Road Ahead With Tradeverifyd

Supply chain statistics allow professionals to stay ahead, optimize their processes, and better understand competitor trends. However, third-party insights are only the first step in your supply chain's journey toward a more resilient experience.

Tradeverifyd offers proactive supply chain risk management solutions that give you greater control of the process, even as it touches each corner of the globe.